スペインの議会下院で、住宅ローンや立ち退き(差押)の法律の変更を議論、採決

PORTADA

Hipotecas y desahucios saltan de la calle al Congreso de los Diputados

Inmaculada de la Vega Madrid 7 FEB 2013 - 14:52 CET

ampliar foto

ampliar foto

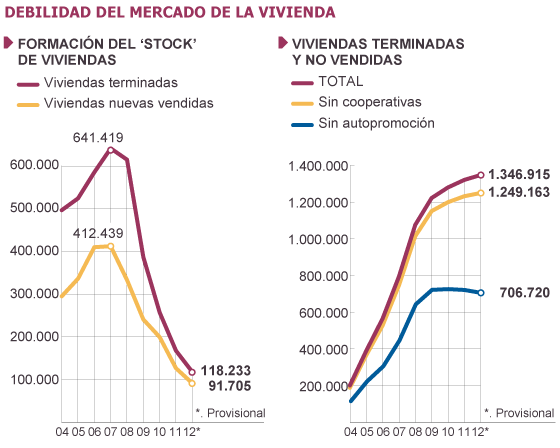

Fuente: Julio Rodríguez, con datos del INE y del Ministerio de Fomento, Federación Hipotecaria Europea, AHE y CGPJ. / EL PAÍS

HOME

Mortgages and foreclosures jump from the street to the Congress of Deputies

Inmaculada de la Vega Madrid 7 FEB 2013 - 14:52 CET

On Tuesday, the PSOE will cede their turn in the House of Representatives for a vote as soon as possible if you take into consideration and therefore whether or not a discussion Popular Legislative Initiative (ILP) to modify the payment in , backed by more than a million signatures, according to the Platform of People Affected by the Mortgage. The promoted along with other associations and unions. It will be at four in the afternoon after taking account of other ILP claiming bullfighting.

And this week has been the attendance of experts in Congress about mortgage reform and evictions. It is at least the third, after a housing commission in 2008 and a subcommittee in 2011 to make inquiries of civic associations.

This appearance occurs in the commission of Economy and Competitiveness, a week after the minister Luis de Guindos announced measures to improve the functioning of the mortgage market and protect vulnerable groups in the context of the discussion of amendments to the entire project Emergency Law to Strengthen Protection of the Mortgage.

Source: Julio Rodriguez, with data from the INE and the Ministry of Development, European Mortgage Federation, AHE and GCJ. / COUNTRY

Guindos proposals show that since the last hearing of experts, something has changed. They are an extension of those adopted in the Code of Good Practice and the two royal decrees of urgent measures adopted in March and November 2012 to support moratorium on the payment of fees, payment in kind, restructure debt or get suspended launch, applicable only to highly vulnerable groups.

Fernando Mendez, exdecano the Association of Registrars is one of the experts who repeated appearance and, in his view "the Government has selected a group of concerned and any selection is arbitrary and discriminatory. A weaker does not help them because they bought and who have incomes below the minimum set is already attached. Customers signed without full knowledge of the consequences will have to clarify it in court and if there are situations of need must be addressed with social policy measures and not measures that undermine the foundations of the system mortgage to the detriment of all, "he explains.

In the street, in the gatherings and is repeated in offices that combat is an imbalance and inequality, not to undermine the system that has allowed mortgage mortgages give a large number of citizens who can mostly meet payments. The default is 3.4%, according to the Spanish Mortgage Association 60% of which was reached in the crisis of '94.

And this percentage, if we stick only to first home, would not even 1%, as explained a few months ago Achutegui Edmundo Rodriguez. A magistrate who, individually or through committees of judges have taken a stand in favor of reforming the foreclosure process and, in some cases, to halt evictions, tired of putting them in front.

To be low delinquencies, the volume of people affected is much larger than in previous crises and their situation dramatically. And those affected and movements such as PAH have demonstrated the imbalance and helplessness between the lender and the debtor in good faith. Imbalances that recognizes his ministry of Economy.

It is not to reduce but to iron guarantees abusive situations that have deserved rejection in the streets and outside our borders. But time is short. And the latest mortgage reforms in 2001 and 2011 returned to improve the position of financial institutions. "The banking lobby is very strong," he says, lowering his voice. But the protests in the street pushing.

Spain is not as singular

In other European countries there is no imbalance between banking and debt, but otherwise Spain has not been an isolated case as a study published in the latest issue of the journal City and Territory, the housing bubble to foreclosures that explains how we got to this situation.

First was the price increase, up to 404% in Ireland between 1987 and 2006, only to fall in the coming years and this also occurred in countries with greater state intervention and extensive presence

social rent. A process that was accompanied by continuing deregulation of financial markets. In parallel, the share in GDP of residential mortgage debt increased by more than 50 points between 1999 and 2010. And, in late 2008, most of Europe into recession and there was a sharp credit crunch. Increased unemployment, defaults and foreclosures in many countries. Between late 2007 and late 2008 increased the percentage of mortgages in arrears of more than three months in Spain 253% and 221% in the U.S..

The authors-A. Etxezarreta, J. Hoekstra, K. Dol and Gala Cano Fuentes, linked to universities of the Basque Country, Murcia and Dutch Delft-allude to the impact of the global financial crisis suffered in varying degrees depending on the country's housing system.

As mortgage credit in Spain, grew between 1996 and 2007 a 738%. And the intended left home purchase 100,000 million in 1999 and exceeded 600,000 million in 2008. The IMF had been warning that the Spanish family exceeded the recommended overhang.

Since 2007, foreclosures soared. Adding rental and property, from less than 26,000 in 2007 to 93,600 in 2010. The evictions have increased but with large differences in percent: ranging from 58% to 390% Asturias and Murcia.

One conclusion is that the volume of foreclosures is related to the degree of state welfare and protection against the risk of unemployment much higher subsidies. Only a few countries have developed specific policies to prevent evictions.

In the UK there is a rescue plan for vulnerable households. And with options like buying the home for 90% of market value. The authors conclude that Spain needs a more equitable mortgage legislation that rules out dramatic situations and a national mortgage rescue. Proposals abound.

The reforms announced last week by Guindos under the bill, incorporate mitigation measures as minorar judges to the family's debt with the bank. Another one, reducing to 12% default interest. The current situation is that "who has a 30-year mortgage and stop paying two installments, all are required to bear interest of 20% or 30% and the procedure expands from 12 to 16 months. This makes your debt is more expensive around 30% at the time the judgment is handed down "explains Mendez proposed default interest similar to those of the Consumer Credit Act or the Exchange Act's check, 2-2 , five times the legal interest rate-less than proposed by Guindos-and review the basis on which it should be calculated from the quotas that have defaulted or, in any case, which fall due during the duration of the trial.

It also calls substantially reduce taxation of foreclosed or equate the auction. "If a foreclosure proceeding bank wins a floor because a buyer has found both the award and the transfer to a third party are exempt from tax. But if it reaches an agreement in lieu of payment to the debtor and seeks someone you buy the floor, the operation becomes more expensive by 20% or 25%, "he says.

Mendez encourage commitment to the mortgagor, after execution, as tenant can continue devoting the amount of your payment to the extinction of credit (antichresis). The creditor banks becomes the administrator and avoids having to provision increasingly, for the asset and the debtor is not left on the street. "The key to the result is that the Bank of Spain to accept the pact anticrético PROVISIONS not", says Mendez.

Another appearing in Congress, Francisca Sauquillo, General Consumer Council, asked, according to Europa Press, a bankruptcy law familiar to indebted households, similar to that of other European countries. Since 2005, we were promised a law of family indebtedness as exists in other European countries.

Coincides again raise the payment in kind, like the judge who asked Vicente Magro expand the circumstances in which the law provides for payment in kind, in a meeting organized by the publisher Francis Lefebvre in which he scored that are accounted 526 evictions a day between premises and homes for sale or rent.

The payment in before anathema, is becoming more common for exceptional situations and is the basis of the popular initiative leading the PAH and has doubled the number of signatures to thrive mandatory.

The lawyer of the PAH, Ada Colau was appearing in one of the Congress and its partner organization, Adria Alemany, stands out as the pressures on the street, add the outside Spain and the active role of judges and regrets , as published COUNTRY, have not been heard. The Socialist Party has called for the expansion of hearings in Congress to accommodate the magistrate José María Fernández Seijo.

Spend the pages

The above raises something ILP

opposing Mortgage Association

Spanish, too

invited to the Congress, and that is that

The Foundation is retroactive. And

also requests the suspension takes the House Street

The mobilization comes antidesahucios Congress of Deputies

IMMACULATE DE LA VEGA

On Tuesday, the PSOE will cede their turn in the House of Representatives for a vote as soon as possible if you take into consideration and therefore whether or not a discussion Popular Legislative Initiative (ILP) to modify the payment in , backed by more than a million signatures, according to the Platform of People Affected by the Mortgage. The promoted along with other associations and unions. It will be at four in the afternoon after taking account of other ILP claiming bullfighting.

And this week has been the attendance of experts in Congress about mortgage reform and evictions. It is at least the third, after a housing commission in 2008 and a subcommittee in 2011 to make inquiries of civic associations.

In the street and ask the experts urgent responses, do not forget the long-term

This appearance occurs in the commission of Economy and Competitiveness, a week after the minister Luis de Guindos announced measures to improve the functioning of the mortgage market and protect vulnerable groups in the context of the discussion of amendments to the entire project Emergency Law to Strengthen Protection of the Mortgage.

Guindos proposals show that since the last hearing of experts, something has changed. They are an extension of those adopted in the Code of Good Practice and the two royal decrees of urgent measures adopted in March and November 2012 to support moratorium on the payment of fees, payment in kind, restructure debt or get suspended launch, applicable only to highly vulnerable groups.

Fernando Mendez, exdecano the Association of Registrars is one of the experts who repeated appearance and, in his view "the Government has selected a group of concerned and any selection is arbitrary and discriminatory. A weaker does not help them because they bought and who have incomes below the minimum set is already attached. Customers signed without full knowledge of the consequences will have to clarify it in court and if there are situations of need must be addressed with social policy measures and not measures that undermine the foundations of the system mortgage to the detriment of all, "he explains.

In the street, in the gatherings and is repeated in offices that combat is an imbalance and inequality, not to undermine the system that has allowed mortgage mortgages give a large number of citizens who can mostly meet payments. The default is 3.4%, according to the Spanish Mortgage Association 60% of which was reached in the crisis of '94.

And this percentage, if we stick only to first home, would not even 1%, as explained a few months ago Achutegui Edmundo Rodriguez. A magistrate who, individually or through committees of judges have taken a stand in favor of reforming the foreclosure process and, in some cases, to halt evictions, tired of putting them in front.

To be low delinquencies, the volume of people affected is much larger than in previous crises and their situation dramatically. And those affected and movements such as PAH have demonstrated the imbalance and helplessness between the lender and the debtor in good faith. Imbalances that recognizes his ministry of Economy.

It is not to reduce but to iron guarantees abusive situations that have deserved rejection in the streets and outside our borders. But time is short. And the latest mortgage reforms in 2001 and 2011 returned to improve the position of financial institutions. "The banking lobby is very strong," he says, lowering his voice. But the protests in the street pushing.

The reforms announced last week by Guindos under the bill, incorporate mitigation measures as minorar judges to the family's debt with the bank. Another one, reducing to 12% default interest. The current situation is that "who has a 30-year mortgage and stop paying two installments, all are required to bear interest of 20% or 30% and the procedure expands from 12 to 16 months. This makes your debt is more expensive around 30% at the time the judgment is handed down "explains Mendez proposed default interest similar to those of the Consumer Credit Act or the Exchange Act's check, 2-2 , five times the legal interest rate-less than proposed by Guindos-and review the basis on which it should be calculated from the quotas that have defaulted or, in any case, which fall due during the duration of the trial.

It also calls substantially reduce taxation of foreclosed or equate the auction. "If a foreclosure proceeding bank wins a floor because a buyer has found both the award and the transfer to a third party are exempt from tax. But if it reaches an agreement in lieu of payment to the debtor and seeks someone you buy the floor, the operation becomes more expensive by 20% or 25%, "he says.

Mendez encourage commitment to the mortgagor, after execution, as tenant can continue devoting the amount of your payment to the extinction of credit (antichresis). The creditor banks becomes the administrator and avoids having to provision increasingly, for the asset and the debtor is not left on the street. "The key to the result is that the Bank of Spain to accept the pact anticrético PROVISIONS not", says Mendez.

Another appearing in Congress, Francisca Sauquillo, General Consumer Council, asked, according to Europa Press, a bankruptcy law familiar to indebted households, similar to that of other European countries. Since 2005, we were promised a law of family indebtedness as exists in other European countries.

Coincides again raise the payment in kind, like the judge who asked Vicente Magro expand the circumstances in which the law provides for payment in kind, in a meeting organized by the publisher Francis Lefebvre in which he scored that are accounted 526 evictions a day between premises and homes for sale or rent.

The payment in before anathema, is becoming more common for exceptional situations and is the basis of the popular initiative leading the PAH and has doubled the number of signatures to thrive mandatory.

The lawyer of the PAH, Ada Colau was appearing in one of the Congress and its partner organization, Adria Alemany, stands out as the pressures on the street, add the outside Spain and the active role of judges and regrets , as published COUNTRY, have not been heard. The Socialist Party has called for the expansion of hearings in Congress to accommodate the magistrate José María Fernández Seijo.

The above ILP raises something that opposes Mortgage Association

Spanish also invited to the Congress, and the Foundation is retroactive. And also sought a moratorium on executions.

And not exhaust all requests of PAH. Alemany explains that when it was written a year and half ago there was the bad bank, the Sareb, and therefore did not demand that the bank foreclosed homes intended for rental. "We have a historic opportunity to create a social housing stock."

Judge Vicente Magro agrees that the fate of homes repossessed by banks are intended for this purpose. Suggests that commitment is agreed that the occupants bear the cost of community and property tax and reduce income almáximo pay for the family.

The debate is open but, apart from addressing a social emergency also asked to avoid changes that once again repeat the liquidity overhang.

ホームページ

住宅ローンや差し押さえは通りからスペイン下院議会へジャンプ

Inmaculadaデラベガマドリード7 FEB 2013 - 午後02時52分CET

そして今週は、住宅ローンの改革と立ち退きに関する議会での専門家の出席となっています。それは2008年の住宅委員会と市民団体に質問させることができる2011年に小委員会の後に、少なくとも第三です。

この外観は大臣ルイス·デ·Guindosは、住宅ローン市場の機能を改善し、プロジェクト全体の改正の議論の文脈に弱者を保護するための措置を発表した一週間後、経済競争力の手数料で発生抵当権の保護を強化するための非常事態法。

出典:INEからデータや開発、欧州モーゲージ連盟、AHEとGCJ省とフリオ·ロドリゲス、。 /国

Guindosの提案は、専門家の最後の公聴会以来、何かが変わったことを示している。彼らは良い実践のための規範で採用され、それらの延長であり、2つの王家は、料金の支払いのモラトリアム、物納をサポートする債務再編または中断ために月と2012年11月に採択された緊急措置の政令非常に脆弱なグループにのみ適用、起動します。

フェルナンド·メンデス、exdecanoレジストラ協会は外観を繰り返すと、彼の見解では "政府は関係者のグループを選択していると、任意の選択が恣意的で差別的である専門家の一人です。彼らが買ったので、弱い彼らを助けないと最小セット以下の所得がすでに接続されている人。結果の完全な知識がなくても、署名されたお客様は、法廷でそれを明確にしなければならないでしょうし、必要性の状況がある場合には、社会政策ではなく、システムの基盤を弱体化させる措置で対処しなければならないすべての不利益に住宅ローンは、 "と彼は説明します。

街頭で、集会で、戦闘が不均衡と不平等、住宅ローンの住宅ローンはほとんど会うことができる市民の多数を与えることができましたシステムを弱体化させるためではないことをオフィスで繰り返される支払い。デフォルトでは'94の危機に達した60%がスペイン語抵当協会によると、3.4%である。

そしてこの割合は、我々が最初に家にだけ固執すれば、たとえ1%ではないだろう、Achuteguiエドムンドロドリゲス数ヶ月前に説明したように。個別に、または裁判官の委員会を介してフロントに置くことの疲れ立ち退きを停止するように、いくつかのケースでは、差し押さえのプロセスの改革に賛成の立場をとっておりました、奉行。

低い延滞であるためには、影響を受ける人々の量は飛躍的に過去の危機とその状況におけるよりもはるかに大きい。と影響を受けるものと、そのようなPAHのような動きは、貸し手と誠意をもって債務者との間の不均衡と無力感を実証している。彼の経済産業省を認識不均衡。

それが短縮されますが、鉄に街頭で我々の国境外拒絶に値した虐待の状況を保証するものではない。しかし、時間は短いです。 2001年と2011年の最新の住宅ローンの改革は、金融機関の地位を向上させるために戻った。 "銀行ロビーは非常に強いです"と、彼は彼の声を下げる、と言う。しかし、街頭での抗議がプッシュ。

スペインは、単数形ではありません

住宅バブルは、他のヨーロッパ諸国では銀行と債務との間に不均衡がありませんが、そうでなければスペインは、ジャーナル·シティとテリトリーの最新号に発表された研究のように孤立した症例はなかった我々はこのような状況になったかを説明差し押さえに。

最初は、今後数年間で下落し、1987年と2006年の間にアイルランドの404%に、価格の上昇であったし、これはまた大きい国家の介入と広範な存在感を持つ国で起こった

社会的な家賃。金融市場の規制緩和を継続することで、同行したプロセス。並行して、住宅ローンの債務のGDPに占めるシェアは1999年から2010年の間に50ポイント以上の増加となりました。そして、2008年後半、景気後退にヨーロッパのほとんどで、シャープな信用収縮があった。多くの国で失業、デフォルトと差し押さえの増加となりました。 2007年後半と2008年後半の間にスペイン253パーセント、米国では221パーセントで三ヶ月以上の延滞住宅ローンの割合を増加させた。

作家·。 Etxezarreta、J.フックストラ、K.国の住宅·システムに応じて様々な程度に苦しんで、世界的な金融危機の影響でDOLとガラカノバスク大学にリンクフエンテス、ムルシアとオランダのデルフト-ほのめかす。

スペインの住宅ローンのように、1996年から2007年の間に738パーセントの増加となりました。と意図された左の家の購入は、1999年の100,000百万円と2008年に60万万人を超えた。 IMFはスペインの家族が推奨オーバーハングを超えたことを警告してきた。

2007年以来、住宅の差し押さえが急増した。 2007未満の26000から2010年には93600に、レンタルやプロパティを追加する。立ち退きは増加したが、パーセントで大きな違いがありました:58%から390パーセントアストゥリアス、ムルシアに至る。

一つの結論は、差し押さえのボリュームが失業はるかに高い補助金のリスクに対する国家の福祉と保護の程度に関係しているということです。ごく一部の国では、立ち退きを防ぐために、具体的な政策を開発しました。

英国では脆弱な世帯の救済策があります。と市場価値の90%のための家を買うようなオプションがあります。著者は、スペインが劇的な状況や国民の住宅ローンの救済を除外してより公平な住宅ローンの立法が必要であることを結論した。提案がたくさんあります。

法案の下Guindosで先週発表された改革は、銀行との家族の借金にminorar裁判官として緩和策を採用しています。 12%の延滞利息を減らすもう一つ、。現在の状況は、30年の住宅ローンを有し、2つの分割払いの支払いを停止誰が "ということで、すべてが20%または30%の利息と手順は12から16ヶ月から展開さを負担する必要があります。これは作るあなたの借金は、 "判決が下された時点で約30%、より高価である消費者信用法又は取引所法のチェックと同様のメンデス提案延滞利息を説明、2-2 、5回法定金利レスで提案よりGuindosと、それが原因で落ちる時にどのような場合に、デフォルト値またはたクォータから計算すべきかの基準を見直す裁判の期間。

それはまた、実質的に抵当流れの課税を削減したり、オークションを同一視呼び出します。 "買い手が見つかったため、差し押さえ手続の銀行が床に勝てば賞および第三者への転送の両方には税金が免除されます。しかし、それは債務者への支払いの代わりに合意に達し、誰かを求める場合あなたが床を購入し、操作は20%以上、25%以上の高価なものとなる "と彼は言う。

メンデスはテナントがクレジットの絶滅(antichresis)にお支払い金額を捧げ続けることができるように、実行された後、抵当権設定者へのコミットメントを奨励しています。債権銀行管理者となり、ますますプロビジョニングする必要がなくなり、資産や債務者は路上に残されていません。 "結果への鍵は、スペインの銀行が協定のanticrético条項を受け入れることではないということです"とメンデス氏は述べています。

別の議会に登場、フランシスカSauquillo、一般消費者委員会は、エウロパ·プレス、他のヨーロッパ諸国と同様のお世話世帯にはおなじみの破産法によると、尋ねた。他のヨーロッパ諸国に存在するとして、2005年以来、私たちは家族の債務の法則を約束された。

ビセンテMagroは彼が占めていることを獲得している出版社フランシス·ルフェーブルが主催する会議で、法律は現物支給に提供している状況を拡大するよう求め裁判官のように、物納を上げる再び一致販売または賃貸のための施設や家庭の間に526立ち退き日。

破門前での支払いは、例外的な状況のために、より一般的になりつつおよびPAHをリードする人気の構想の基礎であり、義務的な繁栄のために署名の数を倍増しているされています。

PAHの弁護士、エイダColau路上で圧力として際立っている議会とそのパートナー組織、アドリアAlemany、のいずれかで表示されてた、外スペインと裁判官と後悔の積極的な役割を追加する、公開国として、聞いていない。社会党は奉行ホセ·マリア·フェルナンデス·成城に対応するために、議会での公聴会の拡大を呼びかけている。

ページを費やす

上記の何かのILPを上げる

抵当に反対

スペイン語、あまりに

議会に招待され、それはつまり

財団は遡及です。と

またサスペンションはハウスストリートを取り要求

動員は、スペイン下院議会antidesahuciosが来る

無原罪のデ·ラ·ベガ

あなたに支払いを変更する議論人気立法イニシアティブ(ILP)のかどうか、したがって考慮するとした場合、火曜日に、PSOEはできるだけ早く投票を下院で自分の順番を譲ることになる、住宅ローンによって影響を受ける人々のプラットフォームに応じて、百万人以上の署名によってバックアップされます。他の団体や労働組合と一緒に推進しました。それは他のILP主張闘牛のアカウントを取った後午後4時となります。

そして今週は、住宅ローンの改革と立ち退きに関する議会での専門家の出席となっています。それは2008年の住宅委員会、市民団体に質問させることができる2011年に小委員会の後に、少なくとも第三です。

路上でと専門家緊急応答を聞いて、長期的なことを忘れないでください

この外観は大臣ルイス·デ·Guindosは、住宅ローン市場の機能を改善し、プロジェクト全体の改正の議論の文脈に弱者を保護するための措置を発表した一週間後、経済競争力の手数料で発生抵当権の保護を強化するための非常事態法。

Guindosの提案は、専門家の最後の公聴会以来、何かが変わったことを示している。彼らは良い実践のための規範で採用され、それらの延長であり、2つの王家は、料金の支払いのモラトリアム、物納をサポートする債務再編または中断ために月と2012年11月に採択された緊急措置の政令非常に脆弱なグループにのみ適用、起動します。

フェルナンド·メンデス、exdecanoレジストラ協会は外観を繰り返すと、彼の見解では "政府は関係者のグループを選択していると、任意の選択が恣意的で差別的である専門家の一人です。彼らが買ったので、弱い彼らを助けないと最小セット以下の所得がすでに接続されている人。結果の完全な知識がなくても、署名されたお客様は、法廷でそれを明確にしなければならないでしょうし、必要性の状況がある場合には、社会政策ではなく、システムの基盤を弱体化させる措置で対処しなければならないすべての不利益に住宅ローンは、 "と彼は説明します。

街頭で、集会で、戦闘が不均衡と不平等、住宅ローンの住宅ローンはほとんど会うことができる市民の多数を与えることができましたシステムを弱体化させるためではないことをオフィスで繰り返される支払い。デフォルトでは'94の危機に達した協会60%がスペイン語抵当によると、3.4%である。

そしてこの割合は、我々が最初に家にだけ固執すれば、たとえ1%ではないだろう、Achuteguiエドムンドロドリゲス数ヶ月前に説明したように。個別に、または裁判官の委員会を介してフロントに置くことの疲れ立ち退きを停止するように、いくつかのケースでは、差し押さえのプロセスの改革に賛成の立場をとっておりました、奉行。

低い延滞であるためには、影響を受ける人々の量は飛躍的に過去の危機とその状況におけるよりもはるかに大きい。と影響を受けるものと、そのようなPAHのような動きは、貸し手と誠意をもって債務者との間の不均衡と無力感を実証している。彼の経済産業省を認識不均衡。

それが短縮されますが、鉄に街頭で我々の国境外拒絶に値した虐待の状況を保証するものではない。しかし、時間は短いです。 2001年と2011年の最新の住宅ローンの改革は、金融機関の地位を向上させるために戻った。 "銀行ロビーは非常に強いです"と、彼は彼の声を下げる、と言う。しかし、街頭での抗議がプッシュ。

法案の下Guindosで先週発表された改革は、銀行との家族の借金にminorar裁判官として緩和策を採用しています。 12%の延滞利息を減らすもう一つ、。現在の状況は、30年の住宅ローンを有し、2つの分割払いの支払いを停止誰が "ということで、すべてが20%または30%の利息と手順は12から16ヶ月から展開さを負担する必要があります。これは作るあなたの借金は、 "判決が下された時点で約30%、より高価である消費者信用法又は取引所法のチェックと同様のメンデス提案延滞利息を説明、2-2 、5回法定金利レスで提案よりGuindosと、それが原因で落ちる時にどのような場合に、デフォルト値またはたクォータから計算すべきかの基準を見直す裁判の期間。

それはまた、実質的に抵当流れの課税を削減したり、オークションを同一視呼び出します。 "買い手が見つかったため、差し押さえ手続の銀行が床に勝てば賞および第三者への転送の両方には税金が免除されます。しかし、それは債務者への支払いの代わりに合意に達し、誰かを求める場合あなたが床を購入し、操作は20%以上、25%以上の高価なものとなる "と彼は言う。

メンデスはテナントがクレジットの絶滅(antichresis)にお支払い金額を捧げ続けることができるように、実行された後、抵当権設定者へのコミットメントを奨励しています。債権銀行管理者となり、ますますプロビジョニングする必要がなくなり、資産や債務者は路上に残されていません。 "結果への鍵は、スペインの銀行が協定のanticrético条項を受け入れることではないということです"とメンデス氏は述べています。

別の議会に登場、フランシスカSauquillo、一般消費者委員会は、エウロパ·プレス、他のヨーロッパ諸国と同様のお世話世帯にはおなじみの破産法によると、尋ねた。他のヨーロッパ諸国に存在するとして、2005年以来、私たちは家族の債務の法則を約束された。

ビセンテMagroは彼が占めていることを獲得している出版社フランシス·ルフェーブルが主催する会議で、法律は現物支給に提供している状況を拡大するよう求め裁判官のように、物納を上げる再び一致販売または賃貸のための施設や家庭の間に526立ち退き日。

破門前での支払いは、例外的な状況のために、より一般的になりつつおよびPAHをリードする人気の構想の基礎であり、義務的な繁栄のために署名の数を倍増しているされています。

PAHの弁護士、エイダColau路上で圧力として際立っている議会とそのパートナー組織、アドリアAlemany、のいずれかで表示されてた、外スペインと裁判官と後悔の積極的な役割を追加する、公開国として、聞いていない。社会党は奉行ホセ·マリア·フェルナンデス·成城に対応するために、議会での公聴会の拡大を呼びかけている。

上記ILPは抵当に反対している何かを発生させ

スペイン語も議会に招待され、財団は遡及です。また、死刑執行のモラトリアムを求めた。

とPAHのすべての要求を排気しない。 Alemanyは、それが一年半前に書かれていたときにバッドバンク、Sarebがあったので、銀行の抵当流れの家は賃貸のために意図することを要求しなかったことを説明しています。 "我々は、社会的な住宅ストックを作成する歴史的な機会を持っています。"

裁判官ビセンテMagroは、銀行による差し押さえ住宅の運命は、この目的のために意図されていることに同意するものとします。居住者が地域社会と固定資産税の費用を負担し、家族のために収入almáximoの給料を減らすことが合意され、そのコミットメントを示唆している。

議論は別としても、再び流動性のオーバーハングを繰り返し変更を避けるように頼ま社会的緊急事態に対処するから、開いているが。

0 件のコメント:

コメントを投稿